Real Estate Investing Using a Home Loan in Estonia - Ultimate Guide

- Romain Armato

- Dec 4, 2021

- 5 min read

Updated: Dec 5, 2021

15 days to obtain a real estate loan and 27 days to make a real estate investment supported by a bank in Estonia! In this article we will see together through a unique case study: the scope of a loan contract, the formalities to be fulfilled (for an entrepreneur and an employee), the interest rates and the negotiation carried out in order to bring you maximum value.

Introduction

Local banks are reluctant to lend to a foreigner, especially if he or she is not yet a resident of Estonia. In most cases, a loan can only be granted if the borrower has a taxable income in Estonia.

In Estonia, the loan rate can be higher than in western countries and adjustable-rate loans are preferred to fixed-rate loans.

There is no need to translate documents for the loan application in Estonia. In other countries, it may be necessary to use the services of a sworn translator.

The figures we will see in this presentation are adapted to my situation and will not necessarily be the ones you will have. They may vary depending on your situation, your project, the bank you are applying to, and the way you present your project.

Case study: our 20th investment in Tallinn

Features: Furnished Studio, New 2019

Surface: 21.7 m² (21.7 sq.ft.)

Location: Tallinn center

Profile of the tenants: Seasonal rental

Steps to follow

1. The Borrower must submit a home loan application (online) and the bank must advise the customer by phone or email (no charge).

2. The Borrower submits the necessary documents for the loan application. The borrower must also order and submit to the bank an appraisal report (at the buyer's expense) to confirm the market value of the property.

3. The bank notifies the borrower of the financing decision and advises the borrower on the terms of the contract to be entered into.

4. The borrower and the bank's representative sign the loan contract digitally.

5. A notarial deed is concluded (notary fees and a tax stamp are paid by the buyer).

6. The Bank pays the loan amount into the borrower's bank account and the borrower pays it to the seller of the property.

7. The borrower must ensure the property and present a valid insurance policy to the bank.

1: Loan application

You can submit a home loan application here: https://www.lhv.ee/en/home-loan/pre-application.

You may need to share the link of the property you want to buy or send more information by email to a bank advisor if the property is off-market

2: Required documents

The borrower's financial situation must be stable to convince a bank in Estonia.

The prerequisites for obtaining a loan in a bank in Estonia are as follows:

For an employee:

Statements of the last 6 months' salary are required for the employee of a startup.

For an employee of an SME: 4 months of salary statements are required (to pass the probation period).

For an entrepreneur:

Account statements proving 6 months of salaries with a minimum of 900 euros net per month.

Income statement less than 2 months old.

A minimum of 2 balance sheets is required.

Evaluation Report

To confirm the market value of the property with the bank, the borrower must also order and submit an appraisal report to the bank (at the buyer's expense).

For various reasons, there may be a price difference between the appraisal report and the seller's asking price. In this case, the buyer must finance the difference.

This document must be signed by you and the expert before sending it to the bank advisor.

3: Financing decision

Here is the first proposal we received (4.2% + 6-month Euribor).

After negotiation, we managed to obtain 3.95% + 6-month Euribor.

In Figures

Contribution: 30% contribution if the property has a commercial designation.

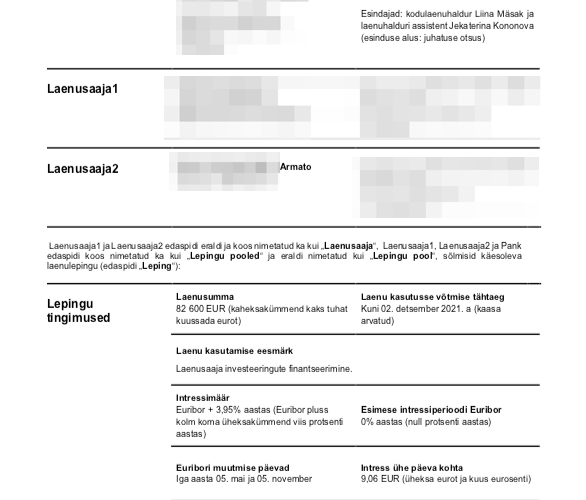

The amount of self-financing is 37.900 €. In our case, the amount of the loan is 82.600 € (70 %);

Rate: 3,95 % + Euribor (6 months) for a rental investment.

The 6-month Euribor rate is the interest rate at which a selection of European banks grant each other loans in euros, the loans having a duration of 6 months.

Loan term: 30 years

Monthly payment: 394 €

Contract fee: 150 € (instead of 300 €)

Early repayment of the loan: free

Deferred payment: only 1 month

Note: the amount of the personal contribution can be 15-20% if the property is for residential use. In this case, the bank can finance up to 85%.

Good to know: in Estonia most new buildings are for commercial use.

Note: the rate is about 2% + Euribor (6 months) if it is a primary residence.

What is Euribor?

Generally, a monthly payment includes the loan repayment (principal) and interest. Interest is a fee that the borrower has to pay to the bank for using the loan amount.

In Estonia it is different:

The interest payment depends on the loan amount as specified in the loan contract, the bank's margin, and the Euribor.

To determine the first monthly repayments, we look at the initial 6-month Euribor: this is the rate that will apply for the first 6 months.

Then, we look at the Euribor 6 months later, and we use it for the next 6 months, and so on until it matures. Thus, the amount of a monthly loan payment changes every six months when the Euribor level changes.

If the Euribor becomes negative, it is considered to be zero. In this case, the monthly loan payment remains the same as initially specified in the loan contract. If it becomes positive then the monthly payment increases.

Therefore, a variable rate loan behaves like a succession of fixed rates that are revealed as they are earned.

Visit https://www.euribor-rates.eu/ to view the historical figures.

In order for the borrower to know the amount of their payment, the bank sends them a new schedule every six months.

4: Loan agreement (November 3rd)

Once the agreement is reached, the bank sends you the loan contract to be digitally signed as well as the payment schedule.

The monthly loan repayments will cover the interest on the loan to a greater extent initially.

Then, the proportion of the principal repaid increases as you go along.

5 & 6: Final signature, payment of notary fees, and transfer of funds (November 4th)

27 days after our request for financing, the transfer of funds and the handing over of the keys took place during the signing of the final act of sale at the notary's office.

In the video below you will see the seller, the bank representative, the real estate agent, us buyers, and the notary in a friendly atmosphere.

For this investment of 120.500 euros, we paid 611 € in notary fees as you can see in the video clip below:

Thank you Estonia !

7: Insurance contract

We have chosen the insurance offered by LHV.

The all-risk insurance for 6,86 € per month. Included :

Fire, natural forces, flooding, damage to the property due to a construction error, burglary, vandalism, other accidents

24 hour home help

Rainwater entering the building

Damage caused by snow or ice build-up on the roof

Failure of household appliances

Insurance against damage caused by the tenant

Replacement home insurance

Loan Repayment Insurance

Rental income insurance

Insurance against damage caused by construction or repair work

Public liability insurance

Timeline:

October 9, 2021: Loan application

October 22, 2021: Signed appraisal report

October 23, 2021: Loan granted

November 3, 2021 : Loan contract signed

November 4, 2021: Final signature at the notary

November 8, 2021: Signed Insurance contract

The process was done online from A to Z !

In October, 21:09 hours were mobilized to realize this investment + 5 hours in November for the signature and the design.

26 hours counted so far.

To go further

NEW: Join our LifeInvest Telegram group: a group of common interests around expatriation and investing abroad.

Choose LifeInvest Case Study™: Private consultation during which we answer your specific and personal questions.

Choose LifeInvest e-residency™: Program to become an Estonian e-citizen and set up your European company remotely through the internet.

Join our LifeInvest Residency™: Program to lower your taxes and increase your purchasing power through expatriation.

Join LifeInvest Heritage™: Program to diversify and build resilient wealth with overseas real estate investment.

LifeInvestment yours,

Romain

Comments